UK Guarantor Loans vs Joint Mortgages: Risks & Benefits

Buying a home in the UK has become increasingly challenging, especially for first-time buyers and younger households. High property prices, strict affordability checks, and large deposit requirements often make it difficult to secure a mortgage on a single income. To overcome these barriers, many buyers consider alternative options such as guarantor loans or joint mortgages.

Both options can help buyers get onto the property ladder, but they come with different risks, responsibilities, and long-term implications. This guide explains how guarantor loans and joint mortgages work in the UK, their benefits and risks, and how to decide which option is right for you in 2025.

What Is a Guarantor Loan or Mortgage?

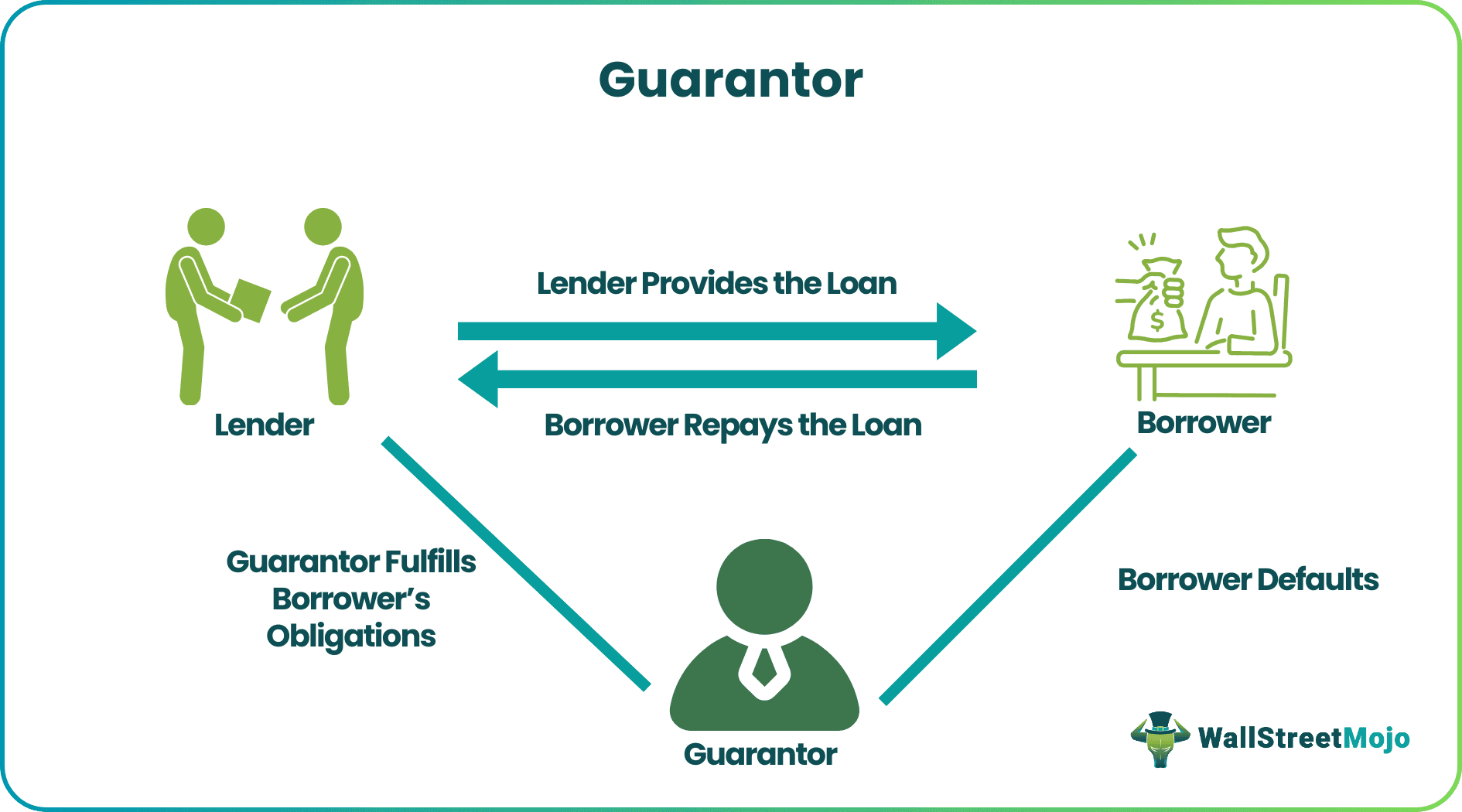

UK Guarantor Loans vs Joint Mortgages: Risks & Benefits A guarantor mortgage involves a third party—usually a parent or close family member—who agrees to take responsibility for the mortgage if the borrower cannot make repayments.

The guarantor does not usually own the property, but their income, savings, or assets provide additional security to the lender.

Who Can Be a Guarantor?

-

Parents or grandparents

-

Close family members

-

In rare cases, close family friends

Lenders require guarantors to have:

-

A strong credit history

-

Stable income or assets

-

No major existing debts

How Guarantor Mortgages Work

-

The buyer applies for a mortgage with a guarantor

-

The guarantor signs a legal agreement

-

If the buyer misses payments, the guarantor must cover them

-

Some lenders secure the guarantor’s savings or property

Guarantor mortgages are often used when a buyer:

-

Has a low income

-

Has a small deposit

-

Has limited credit history

Benefits of Guarantor Loans

1. Easier Mortgage Approval

UK Guarantor Loans vs Joint Mortgages: Risks & Benefits Guarantor support increases lender confidence, making approval more likely.

2. Higher Borrowing Potential

Buyers may be able to borrow more than they could on their own.

3. Lower Deposit Requirements

Some guarantor mortgages allow deposits as low as 5%.

4. Faster Route to Homeownership

Ideal for first-time buyers struggling with affordability.

Risks of Guarantor Loans

1. Financial Risk to the Guarantor

UK Guarantor Loans vs Joint Mortgages: Risks & Benefits If repayments are missed, the guarantor must pay. In some cases, their home or savings could be at risk.

2. Impact on Guarantor’s Credit

Missed payments can harm the guarantor’s credit score.

3. Reduced Borrowing Power for Guarantor

The guarantor may find it harder to get loans or mortgages themselves.

4. Family Strain

Money issues can create tension if repayment problems arise.

What Is a Joint Mortgage?

UK Guarantor Loans vs Joint Mortgages: Risks & Benefits A joint mortgage is when two or more people apply for a mortgage together and share responsibility for repayments.

All borrowers named on the mortgage are jointly and severally liable, meaning each person is responsible for the full mortgage, not just their share.

Types of Joint Mortgages in the UK

1. Joint Borrower, Joint Owner

-

All borrowers own the property

-

Common for couples or partners

2. Joint Borrower, Sole Owner (JBSP)

-

Parents help with income

-

Only the main buyer owns the property

-

Popular with first-time buyers

How Joint Mortgages Work

-

Multiple incomes are combined

-

Borrowing capacity increases

-

All named borrowers are legally responsible

Joint mortgages are often used by:

-

Couples buying together

-

Family members pooling income

-

Buyers using the JBSP model

Benefits of Joint Mortgages

1. Increased Affordability

UK Guarantor Loans vs Joint Mortgages: Risks & Benefits Combining incomes allows buyers to borrow more.

2. Shared Financial Responsibility

Monthly repayments are split between borrowers.

3. No Need for a Guarantor

Everyone involved is an equal borrower.

4. More Mortgage Options

Joint mortgages are widely available across lenders.

Risks of Joint Mortgages

1. Shared Liability

If one borrower cannot pay, the others must cover the full amount.

2. Credit Score Impact

Missed payments affect everyone’s credit history.

3. Ownership Complications

Selling or remortgaging requires agreement from all parties.

4. Relationship Breakdown Risks

Separation or disputes can complicate property ownership.

Guarantor Loans vs Joint Mortgages: Key Differences

| Feature | Guarantor Loan | Joint Mortgage |

|---|---|---|

| Ownership | Borrower only | Shared or sole |

| Liability | Guarantor covers if needed | All borrowers fully liable |

| Risk Level | Higher for guarantor | Shared among borrowers |

| Deposit Needed | Often lower | Usually higher |

| Family Involvement | Financial backup | Direct involvement |

Which Option Is Better for First-Time Buyers?

When a Guarantor Loan Is Better

-

You want full ownership

-

Parents are financially strong

-

You expect income to rise soon

-

You need help temporarily

When a Joint Mortgage Is Better

-

Buying with a partner

-

Sharing costs long-term

-

Comfortable with shared ownership

-

Stable joint income

Tax and Legal Considerations

-

Joint owners may face Capital Gains Tax on second properties

-

Guarantors usually have no tax liability

-

Legal advice is strongly recommended

Can You Remove a Guarantor Later?

Yes. Once:

-

Your income increases

-

Your loan-to-value improves

-

You build a good repayment history

You can remortgage and remove the guarantor.

Can You Switch from Joint to Sole Mortgage?

Yes, but:

-

You must meet affordability checks alone

-

Legal and remortgage fees apply

Impact on Credit Scores

-

Both options affect credit history

-

Missed payments harm all responsible parties

-

On-time payments build positive credit

Should You Use a Mortgage Broker?

A mortgage broker can:

-

Compare guarantor and joint options

-

Explain lender-specific rules

-

Protect family interests

-

Find specialist lenders

Many UK brokers offer free initial advice.

2025 Market Outlook

In 2025:

-

Lenders remain cautious

-

Family-assisted mortgages are growing

-

Affordability checks are still strict

Both guarantor loans and joint mortgages remain valuable tools, but careful planning is essential.

Final Verdict: Which Is Right for You?

UK Guarantor Loans vs Joint Mortgages: Risks & Benefits There is no one-size-fits-all answer.

Choose a Guarantor Loan if:

✔ You want sole ownership

✔ Family support is available

✔ You expect future income growth

Choose a Joint Mortgage if:

✔ You’re buying with a partner

✔ You want shared responsibility

✔ Long-term collaboration is comfortable

READ ALSO :